info@libristo.bg

Ще ви отговорим до 24 часа

Безплатна доставка със Speedy над 129 лв

Box Now 9 лв

Speedy office 11 лв

Speedy 13 лв

ЕКОНТ 6 лв

Еконтомат/Офис на Еконт 6 лв

Контакт

Контакт Как се пазарува?

Как се пазарува?

Помощ

Доставка

Box Now 9 лв

Speedy office 11 лв

Speedy 13 лв

ЕКОНТ 6 лв

Еконтомат/Офис на Еконт 6 лв

Безплатна доставка със Speedy над 129 лв

Наръчник за пазаруване

Тук сме за Вас!

info@libristo.bg

Моят акаунт

Станете част от общност от любители на книгите от цял свят и получавате много предимства.

Създай на безплатен акаунт

▸

Празна :-(

0

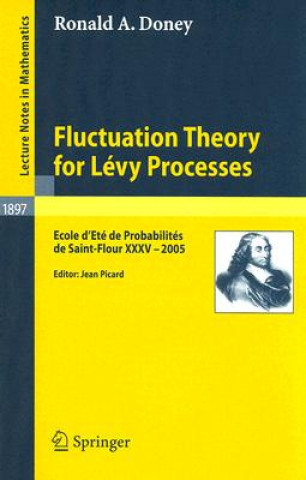

Fluctuation Theory for Lévy Processes

Език

Английски език

Английски език

Английски език

Книга

С меки корици

Lévy processes, that is, processes in continuous time with stationary and independent increments, fo...

Цялото описание

Код Либристо: 05274063

?

164 b

164 b

164 b

129

лв

Външен склад в ограничено количество

Изпращаме след 12-17 дни

30 дни за връщане на стоката

Може би ще Ви заинтересува

/

С твърди корици

/

С твърди корици

142

лв

142

лв

Lévy processes, that is, processes in continuous time with stationary and independent increments, form a flexible class of models, which have been applied to the study of storage processes, insurance risk, queues, turbulence, laser cooling, and of course finance, where they include particularly important examples having "heavy tails." Their sample path behaviour poses a variety of challenging and fascinating problems, which are addressed in detail.

Информация за книгата

Пълно заглавие

Fluctuation Theory for Lévy Processes

Автор

Ronald A. Doney

Език

Английски език

Английски език

Корици

Книга - С меки корици

Дата на издаване

2007

Брой страници

155

Баркод

9783540485100

ISBN

3540485104

Код Либристо

05274063

Издателство

Springer, Berlin

Тегло

254

Размери

158 x 232 x 10