Контакт

Контакт Как се пазарува?

Как се пазарува?Доставка

Наръчник за пазаруване

Limit Order Books

Английски език

Английски език

144 b

144 b

30 дни за връщане на стоката

Може би ще Ви заинтересува

/

С твърди корици

/

С твърди корици

141

лв

141

лв

/

С меки корици

109

лв

/

С меки корици

109

лв

/

С меки корици

38

лв

/

С меки корици

38

лв

/

С твърди корици

335

лв

/

С твърди корици

335

лв

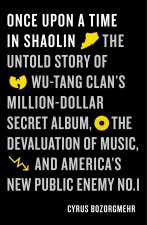

This book discusses several models of limit order books and introduces a general, flexible open-source library, useful to readers studying trading strategies in order-driven markets. It begins by assessing relevant empirical data, moves on to mathematical models, in order to reproduce observed properties, and finally presents a framework for numerical simulations. It covers some of the important modelling techniques in detail, including agent-based modelling, advanced modelling of limit order books based on Hawkes processes, Jaisson and Rosenbaum theories, and LLOB models. The book also provides in-depth coverage of simulation techniques, such as numerical simulation and the limit order book simulator. It will be useful to graduate students in the fields of econophysics, financial mathematics, actuarial mathematics and high frequency financial data.

Информация за книгата

Английски език