Контакт

Контакт Как се пазарува?

Как се пазарува?Доставка

Наръчник за пазаруване

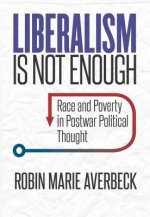

Real Exchange Rate Movements

An Econometric Investigation into Causes of Fluctuations in Some Dollar Real Exchange Rates

Немски език

Немски език

132 b

132 b

До 30 дни за връщане на стоки

Клиентите са закупили също

/

/

С меки корици

С меки корици

34.01

€

66.52 лв

34.01

€

66.52 лв

/

С меки корици

8.53

€

16.67 лв

/

С меки корици

8.53

€

16.67 лв

/

С твърди корици

167.55

€

327.71 лв

/

С твърди корици

167.55

€

327.71 лв

/

С меки корици

19.33

€

37.81 лв

/

С меки корици

19.33

€

37.81 лв

/

С меки корици

29.52

€

57.73 лв

/

С меки корици

29.52

€

57.73 лв

/

С меки корици

34.22

€

66.93 лв

/

С меки корици

34.22

€

66.93 лв

One aim of this book is to examine the causes of fluctuations in the mark/dollar, pound/dollar, and yen/dollar real exchange rates for the period 1972-1994 with quarterly data to determine appropriate policy recommendations to reduce these movements. A second aim is to investigate whether the three real exchange rates are covariance-stationary or not and to which extent they are covariance-stationary, respectively. These aims are reached by using a two-country overshooting model for real exchange rates with real government expenditure and by applying Johansen's maximum likelihood cointegration procedure and a factor model of Gonzalo and Granger to this model.

Информация за книгата

Немски език

Категории

Подарете тази книга днес

Лесно е

1 Добавете книгата в количката си и изберете Доставка като подарък 2 В замяна ще ви изпратим ваучер 3 Книгата ще пристигне на адреса на получателяМоже би ще Ви заинтересува

/

С твърди корици

17.16

€

33.56 лв

/

С твърди корици

17.16

€

33.56 лв

/

С меки корици

65.86

€

128.81 лв

/

С меки корици

65.86

€

128.81 лв

/

С меки корици

27.50

€

53.78 лв

/

С меки корици

27.50

€

53.78 лв

/

С меки корици

46.32

€

90.59 лв

/

С меки корици

46.32

€

90.59 лв

Здравейте! Аз съм Libroamiko, вашият книжен съветник.

Как мога да ви помогна?